Seller Closing Cost Calculator

Estimate everything a home seller pays at the closing table – agent commission, transfer or excise tax, title and escrow, prorated property taxes, buyer concessions, and mortgage payoff – then see your true net proceeds.

🎯Real Seller Scenarios

📝Sale & Cost Inputs

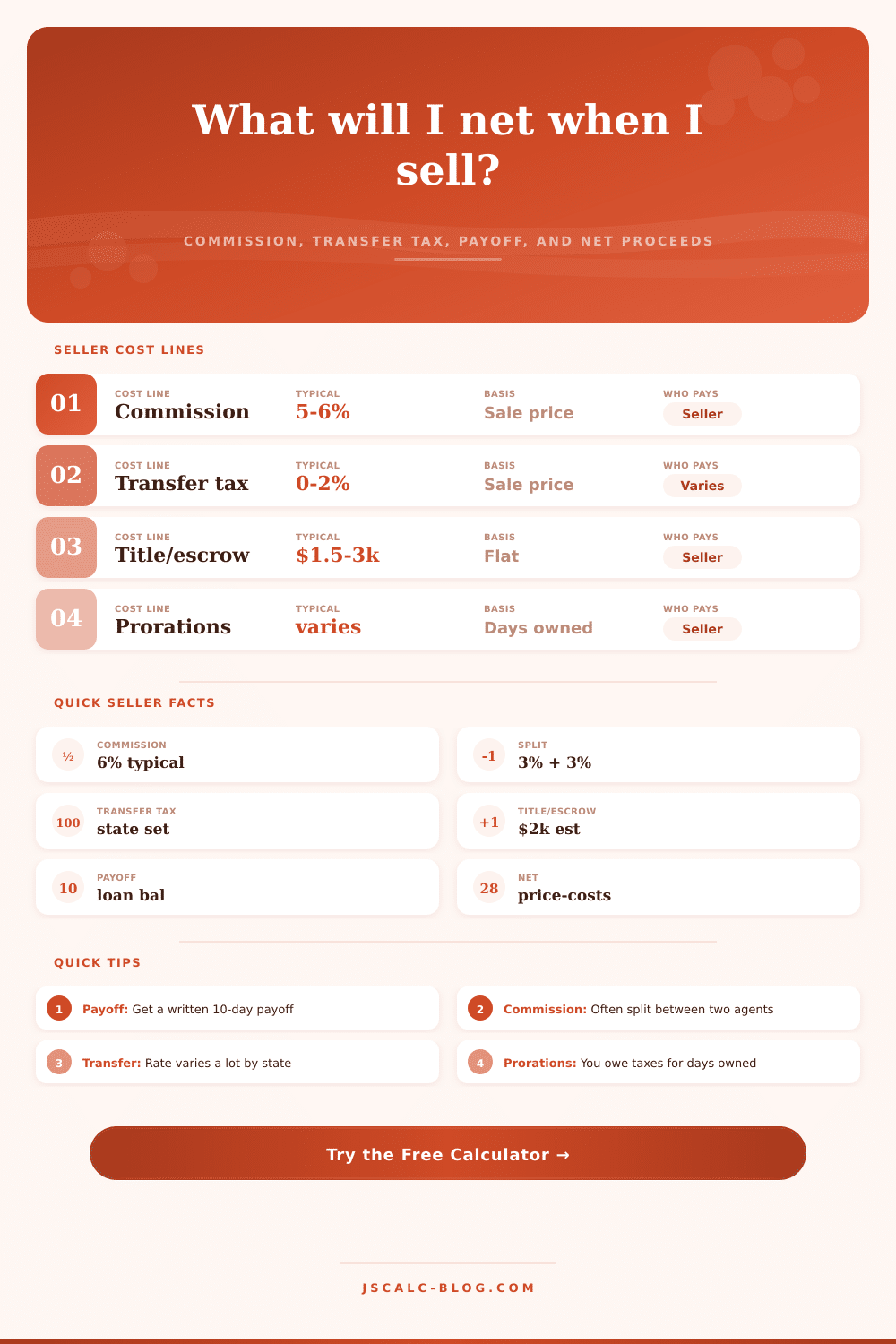

Remaining principal you must pay off from proceeds.

Typically split roughly 3% listing + 3% buyer agent.

Used when method is percent of sale price.

Used when method is flat dollar amount.

Your share of taxes for the days you owned the home.

Credits toward the buyer's closing costs or repairs.

Used to estimate gross gain, not a tax opinion.

🔢Net Proceeds Snapshot

📋Typical Seller Cost Components

| Cost Line | Typical Range | How It Is Figured | Notes |

|---|---|---|---|

| Real estate commission | 5% to 6% of price | Sale price × rate | Largest line for most sellers |

| Transfer / excise tax | 0% to 2% of price | Price × rate or flat | Set by state, county, or city |

| Title insurance & escrow | $1,500 to $3,000 | Flat or price-scaled | Owner policy custom varies by area |

| Prorated property taxes | Depends on due dates | Annual tax × days owned / 365 | Seller covers days before closing |

| Buyer concessions | 0% to 3% of price | Negotiated credit | Helps buyer with closing costs |

| Other fees | $300 to $1,200 | HOA transfer, warranty, recording | Small but easy to overlook |

🤝Commission Split Reference

| Total Rate | Listing Side | Buyer Side | On $500k |

|---|---|---|---|

| 4.0% | 2.0% | 2.0% | $20,000 |

| 5.0% | 2.5% | 2.5% | $25,000 |

| 5.5% | 2.75% | 2.75% | $27,500 |

| 6.0% | 3.0% | 3.0% | $30,000 |

| 0.0% (FSBO) | 0.0% | 0.0% | $0 |

🗺Transfer Tax By State (Examples)

| State / Area | Seller Rate | Basis | On $500k |

|---|---|---|---|

| No transfer tax | 0.00% | None | $0 |

| Low-rate example | 0.10% | Sale price | $500 |

| Mid-rate example | 0.60% | Sale price | $3,000 |

| Higher-rate example | 1.10% | Sale price | $5,500 |

| High-cost metro | 1.80% | Sale price | $9,000 |

Rates are illustrative. Confirm your exact local transfer, excise, or documentary stamp rate with your title company or closing attorney.

🗂Net Proceeds Comparison Grid

| Scenario | Sale Price | Commission | Payoff | Total Costs | Net Proceeds |

|---|---|---|---|---|---|

| $400k, 6%, low tax | $400,000 | $24,000 | $220,000 | $29,600 | $150,400 |

| $500k standard | $500,000 | $30,000 | $300,000 | $37,200 | $162,800 |

| $650k luxury | $650,000 | $39,000 | $390,000 | $50,300 | $209,700 |

| FSBO no agent | $450,000 | $0 | $250,000 | $6,100 | $193,900 |

| Cash sale, low fees | $420,000 | $25,200 | $0 | $29,700 | $390,300 |

| High-tax state | $500,000 | $30,000 | $280,000 | $45,200 | $174,800 |

Rows are worked examples so you can sanity-check the calculator output against familiar shapes.

⚙Full Formula Breakdown

📊Net Proceeds Worksheet

| Step | Line Item | Sign | Amount |

|---|---|---|---|

| Enter values above to build your net proceeds worksheet. | |||

💡Practical Seller Tips

Now, you’re standing in your living room picturing handing over the keys, and depositing a check into your account. Until you remember: The sale price isn’t the start; it’s the starting line for an extremely expensive race. Closing costs represent the invisible tax structure of selling. They’re something most sellers only consider when trying to get the biggest bidder, completly neglecting what will happen once they hand over the keys.

If you don’t look at each line item up-front, the difference between headline offer and actual cash in your bank account can be shocking. Once you plug in your roof size and your rainfall, the math happens for you (since it spares you from doing conversions or coefficient guessing). It then break down the problems that eat away at your equity.

How Much Money Will You Really Get?

The biggest chunk will typically be agent commission: a half-million dollar house sold at the usual rate of six percent will hand you over to another person thirty thousand dollars before you’ve even thought about fees or taxes. That covers both sides of representation (the listing side and buyer’s side). It is rarely negotiable in the moment, though it is always worth asking what the split will look like before you sign on the dotted line.

Adding to the complexity are the wildly different transfer taxes, depending on where you live. While some states has no such tax, other locations have rates that will make you think “what a penalty for moving my wealth!” The tool allows you to toggle between a flat fee or a percentage calculation based off your jurisdiction’s rules. Don’t assume there is a county or city surcharge on top of the state tax. You must check if your local area charges an extra fee beyond what the state requires. Municipal fees are often right there in plain sight until you see them on final settlement statement.

Give a lot of weight to title insurance and escrow services. Yes, these are necessary to clean up the transfer of ownership, this is a fair price to avoid legal headaches down the road, but they still suck away from your proceeds.

Many folks get tripped up by proration, which is why these is more time-based than flat fee items. Even though your property tax bill won’t arrive for several months, you’ll still owe property taxes for any days that fall within current tax year while you’re the owner. Although the calculator uses average yearly burdens as an estimate, your specific figure will vary significant depending upon where you live and how assessments is done.

A third wrinkle is buyer concessions. Did you agree to credit the buyer for his/her own repairs or closing costs? That money’s coming straight from your pocket. While it may seal a sale in a slow market, it also takes money away from what you has to walk away with.

Your mortgage anchors your equity down. Until the bank is paid, there’s no profit in the pot. To avoid any surprises (prepayment penalties and accrued interest can pop up), get a written payoff figure from your lender with a ten-day estimate. More times than not, this number is higher then you remember. This step shows you why your mortgage balance are higher than you expected.

Small items such as home warranties and HOA transfers don’t seem big enough to matter…until you add them all up. If ignored, then your final check will disappoint because it’ll be skinnier than expected. Because of that, I really like this breakdown from the page, which visually explains how various situations plays into the bottom line:

When looking at for-sale-by-owners vs. Working with an agent, it’s clear to see what kind of fee structure is required, and deserved!; by pro rep services. At the same time, as the table shows, there is also total costs associated with luxurius properties, although the percentages might remain the same.

Knowing all this will help put you in the right frame of mind ahead of list day one. Selling a house is an emotional transaction, but it also has a cold precision in its financial mechanics. The market conditions are outside of your control, but the cost structure is something that you should of have some control over.

If you want to sell faster, negotiate better, or determine which upgrades yield higher returns, understanding exactly where the money flows will help you make smarter decisions. Don’t guess at your net proceeds, few things account for all the hidden layers of fees/taxes accumulating in the background. But here’s the trick: Before you get excited by a high offer, it helps to understand what exactly they’re measuring.

Because that’s where people screw up. They celebrate the bid and then they forget the bill. So begin with the math and end with clarity, not shock. You want to know exactly how much money ends up in your pocket once everyone else gets paid.