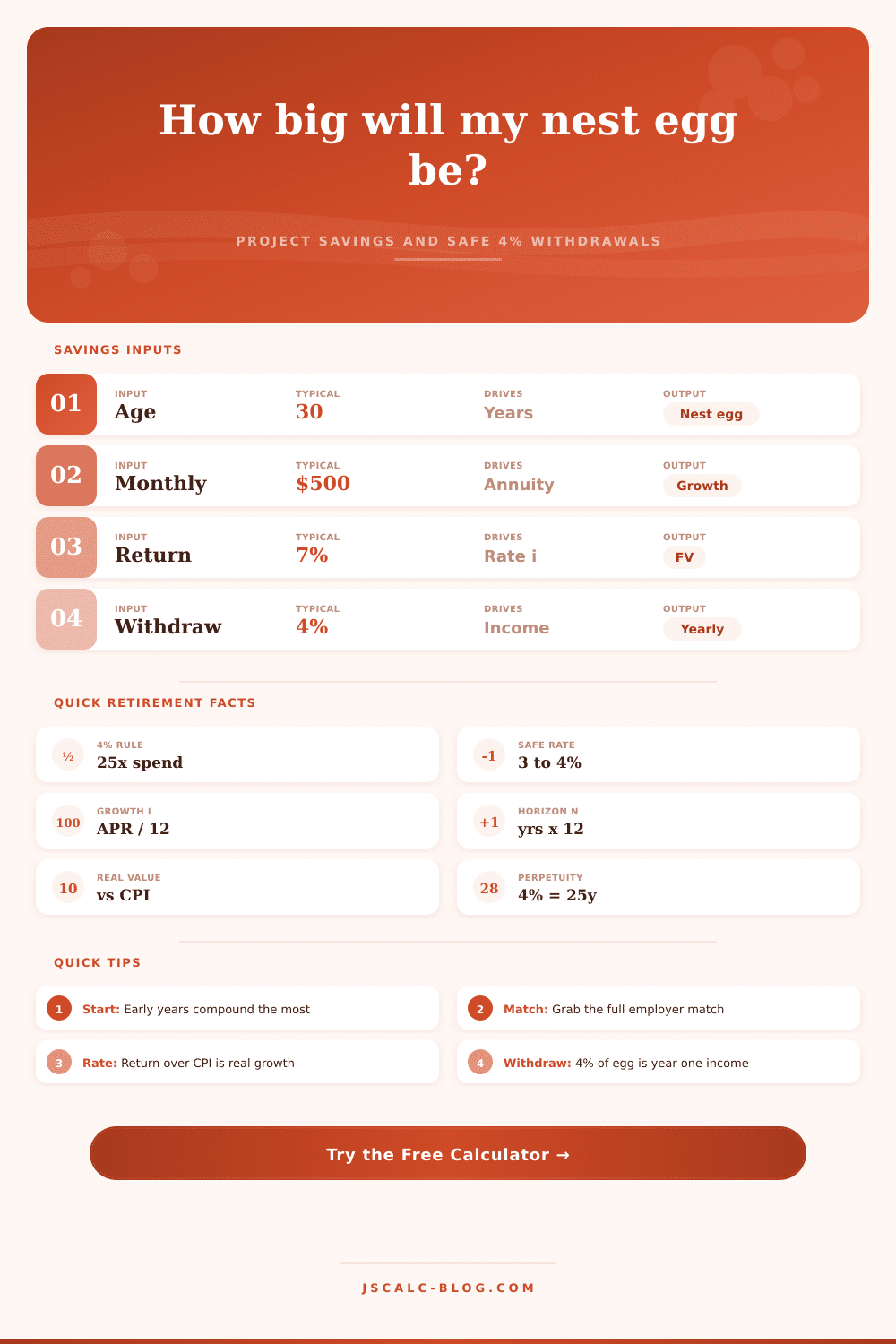

Retirement Savings Calculator

Project your future nest egg from current savings and monthly contributions using compound time-value-of-money growth, then estimate sustainable annual income with the 4% safe withdrawal rule.

🎯Real Savings Presets

📝Your Savings Plan

Raises your monthly deposit each year, e.g. with pay raises.

🔢Formula Snapshot

📊Year-by-Year Projected Balance

| Age | Year # | Start Balance | Contributed | Growth | End Balance |

|---|---|---|---|---|---|

| Enter values above to project your balance year by year. | |||||

💸Withdrawal Rate to Annual Income

| Withdrawal Rate | Nest Egg Multiple | Annual Income | Monthly Income | Risk Note |

|---|---|---|---|---|

| The withdrawal reference table appears after calculation. | ||||

📈Contribution vs Nest Egg by Start Age

| Start Age | Years to 65 | Monthly Saved | Total Put In | Nest Egg at 65 | Growth Multiple |

|---|---|---|---|---|---|

| The start-age comparison appears after calculation. | |||||

🌍Inflation-Adjusted Purchasing Power

| Return | Nest Egg (Nominal) | CPI Factor | Real Value Today | Real 4% Income | Buying Power |

|---|---|---|---|---|---|

| The purchasing-power comparison appears after calculation. | |||||

⚙Full Formula Breakdown

📋Reference Values

| Item | Common Entry | How It Is Used | Effect On Nest Egg |

|---|---|---|---|

| Current age | 25 to 55 | Sets years N until retirement | More years means more compounding |

| Monthly contribution | $200 to $2,000 | Annuity payment each month | Scales the deposit portion directly |

| Return before | 5% to 9% | Growth rate i during saving | Higher rate compounds faster |

| Inflation / CPI | 2% to 4% | Discounts to today's dollars | Lowers real buying power, not nominal |

| Withdrawal rate | 3% to 4% | Turns egg into yearly income | Higher rate spends the egg faster |

💡Practical Retirement Tips

Time matters, too, when it comes to retirement. Far more then raw cash savings. Compound interest, as we learned above, is very friendly towards patient people who saves small amounts now; it’s less friendly toward impatient people who make big bucks but save less often or later in their lives. (Think of the difference between working full-time in your twenties versus working part-time in your fifties.)

Yes, you could catch up by contributing thousands per month later in life, but that won’t bend the curve back quite far enough to compensate for decades of missed compounding. Plug in your starting age and monthly savings amount, and let the calculator do its thing. You don’t need to guess the relative value of a dollar saved today versus one saved a decade from now.

Time Matters for Retirement

It’s just a simple concept. Begin with your starting balance, add your monthly contribution, and finally multiply by annual return rate over many years. But everyone seem to screw this up. The key: Your initial contributions will compound rapidly whereas your final few contributions don’t even have time to catch there breath. Compounding will double your money about every decade if you earns an average of seven percent annually.

Initially you won’t notice this compounding, but as your balance increases, it becomes the major factor in your portfolio. Most folks obsess about how much they’re contributing because it makes them feel like they’re taking some sort of action, but the true power lie with those silent dollars accumulating interest while sitting idle in your account.

Next, determine what is a reasonable return for your circumstances. A diversified stock portfolio over time will generate roughly seven percent, but that’s the average of both good years and bad years. This app allows you to customize the percentage to match your risk tolerance level. You can see what a conservative portfolio with a 4 percent return would look like different than a more aggressive portfolio at a nine percent return.

If your returns are lower, then you’ll require a bigger nest egg to reach your desired income level… Forcing you into one of two choices: Save more, or wait longer until retirement. There’s no escaping, it’s a tradeoff between volatility now and security later. You can’t just plug in the highest number possible and cross your fingers; market crashes invariably occurs at the most inconvenient moments, such as just prior to when you’re planning to stop working.

After projecting your total nest egg, then what? How quickly can you safely withdraw that pile of money without running out? That’s where the four percent rule enters into play. It’s a basic withdrawal rule of thumb for making safe withdrawals from your portfolio: Withdraw four percent of your portfolio annually, adjusted for inflation. Your money will last at least thirty years, riding through multiple market cycles.

Why does it work? You are leaving the other ninety-six percent invested, creating growth to hopefully exceed inflation and pay for the rest. That’s the theory behind the four percent rule. The calculator uses this percentage to estimate your first-year income. This real-world figure shows whether or not you’ll be able to maintain the lifestyle you want with your savings.

Maybe you discover that it’s less than you expected. Good! It’s better to know before you retire. It also adjusts for inflation. Most projections fail to do this, which is why they’re usually late. Yes, a million dollars seems great. But unless inflation remains constant, your million bucks won’t purchase as much 30 years from now.

The tool lets you see how much your future balance would be, in today’s purchasing power. That makes a huge difference: We humans are hard-wired to think in “nominal” (big-number) terms instead of “real” (what it actualy buys me) terms. By knowing the difference, you’ll set better goals, and you won’t be disappointed when you retire to find that your big account balance doesn’t feel nearly as full after all.

If I could go back, I would of loved for my first savings to be 20+ years ago. But if I can’t go back, then the next-best time is today. You don’t need a huge lump sum upfront (or even a clear plan). A little bit of saving every month will compound over time, far quicker than you might think.

Run some what-if-scenarios using this calculator and observe how adjusting your retirement age or contributing slightly more money each year alters the result. This isn’t as much about reaching a specific dollar amount; rather, it’s about learning the connection between your current habits and your future freedom. Time is your most precious possession. Treat it that way.