Debt to Income Ratio Calculator

Itemize every monthly debt, compute your front-end (housing) and back-end (total) DTI from gross income, and rate the result against conventional, FHA, VA, USDA, and qualified-mortgage lender thresholds.

🎯Real DTI Presets

💵Income

Applies to both income boxes below.

Use pre-tax (gross) income, not take-home pay.

Spouse or joint applicant; leave 0 if none.

📝Itemized Monthly Debts

PITI + HOA if you own; counts toward front-end.

Use minimum due, not the full balance.

Excluding sets front-end DTI to 0%.

🔢Formula Snapshot

📋Itemized Debt Summary

| Debt Category | Monthly Payment | Share of Total Debt | Share of Gross Income | Counts Toward |

|---|---|---|---|---|

| Enter values above to calculate the itemized debt summary. | ||||

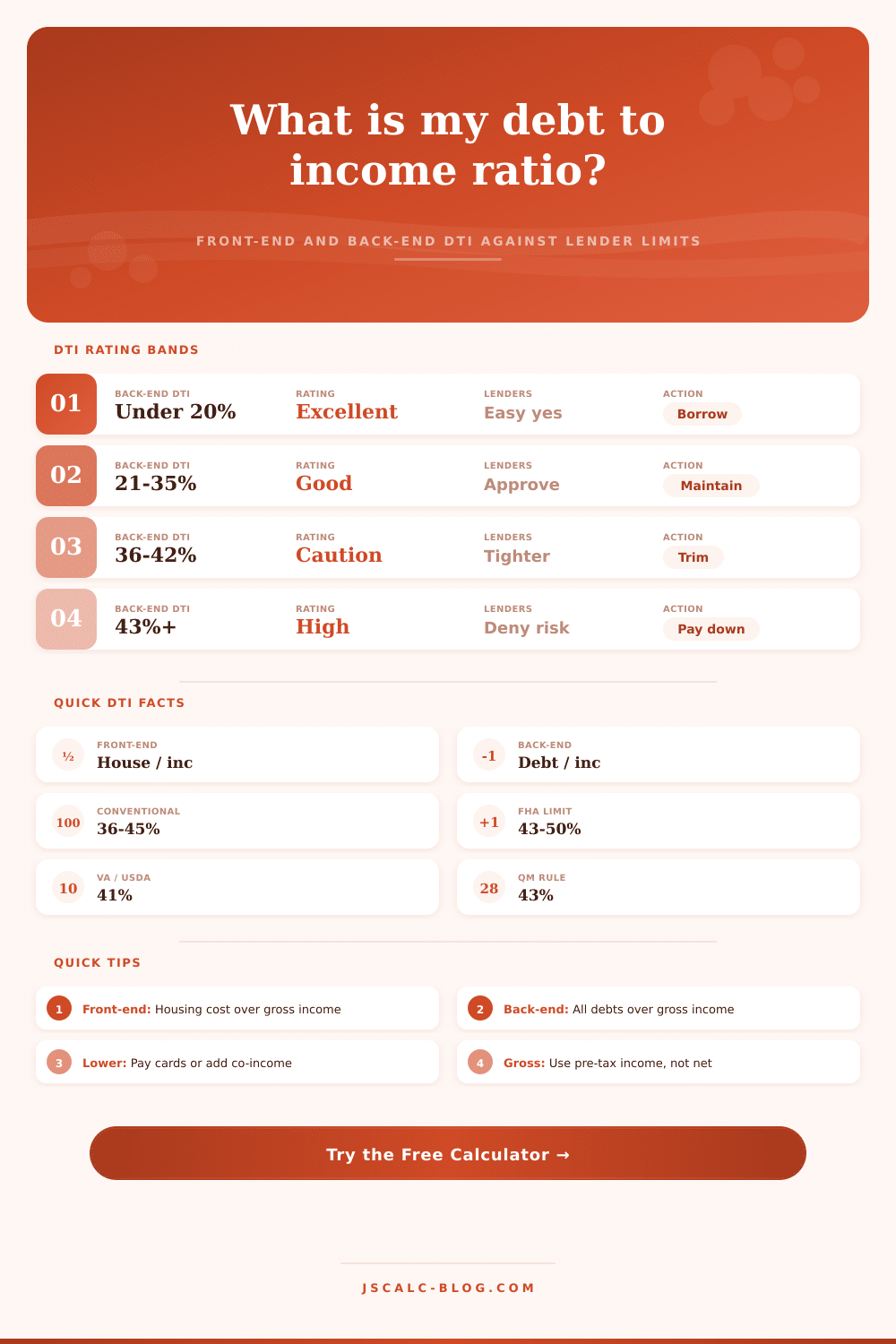

📊DTI Rating Scale

| Back-end DTI Range | Rating | What Lenders See | Recommended Action |

|---|---|---|---|

| 0% – 20% | Excellent | Very low risk, easiest approvals | Room to borrow or invest |

| 21% – 35% | Good / Manageable | Comfortable, most loans approve | Maintain and build savings |

| 36% – 42% | Caution | Acceptable but scrutinized | Trim revolving balances |

| 43% – 49% | High | Near limits, needs compensating factors | Pay down debt before applying |

| 50% and above | Critical | Most lenders decline | Restructure or reduce debt |

🏦Lender Threshold Guide

| Loan Program | Front-end Guide | Back-end Max | Notes |

|---|---|---|---|

| Conventional (Fannie/Freddie) | 28% | 36% – 45% | Up to 45%–50% with strong credit and reserves |

| FHA | 31% | 43% – 50% | Above 43% needs compensating factors |

| VA (Veterans Affairs) | N/A | 41% | Residual income test can allow higher |

| USDA (Rural Development) | 29% | 41% | Waivers possible with credit score 680+ |

| Qualified Mortgage (QM) | N/A | 43% | Legal safe-harbor ceiling for lenders |

| Jumbo / Portfolio | 28% | 36% – 43% | Stricter; larger reserves required |

🗂Borrower Comparison Grid

| Profile | Gross Income | Housing | Other Debt | Back-end DTI | Standing |

|---|---|---|---|---|---|

| Debt-free saver | $6,000/mo | $0 | $0 | 0% | Excellent |

| Renter, light debt | $5,000/mo | $1,400 | $250 | 33% | Good |

| Homeowner, balanced | $7,500/mo | $1,900 | $800 | 36% | Caution |

| Car + cards heavy | $5,500/mo | $1,500 | $1,050 | 46% | High |

| Student debt heavy | $4,800/mo | $1,300 | $1,050 | 49% | High |

| Overextended | $5,000/mo | $1,700 | $1,150 | 57% | Critical |

| Dual income pro | $11,000/mo | $2,600 | $900 | 32% | Good |

💰Income-to-Max-Debt Reference

| Gross Monthly Income | Max Debt @ 28% | Max Debt @ 36% | Max Debt @ 43% |

|---|---|---|---|

| Reference table appears after calculation. | |||

⚙Full Formula Breakdown

💡Practical DTI Tips

When a mortgage application slows down, it’s rarely due to the home itself. Rather, there’s some negative-looking number sitting in that underwriter’s file. That number would of been your debt-to-income ratio (or DTI). This is key number a lender will use to decide whether you can afford the loan.

You might think that having good credit score ensures approval. While a solid credit history show your ability to repay previous debts, a low debt-to-income ratio shows that you’ll have plenty of cash flow remaining after taking on this new one. In other words, it demonstrates that your existing expenses aren’t more than what your current income allows with room for a new mortgage payment.

How Your Debt Affects Your Mortgage

Here’s where the calculator on this page comes in handy. It splits your finances into two bucket. Your front-end ratio represents housing costs as a percentage of your gross monthly income. Your back-end ratio include everything else, such as credit card minimums, student loans, car payments and more. Banks care most about latter, since that shows them how stretched you are based off all recurring expenses.

Plug your numbers into the tool above and it’ll diagnose your level of financial flexibility. If your back-end DTI is below 20%, you’re low-risk to banks and therefore usually get better rates and faster approvals. If you’re well below the line, congratulations! You have some negotiating power. If you’re near the limit, don’t expect any favors.

But first let’s address what qualifies as debt. Many people mistakenly believe that revolving balances (e.g., on a credit card) are less serious than installment payments if they’re paid in full each month. Banks don’t see it that way. When calculating your debt-to-income ratio, they’ll use your minimum monthly payment instead of the total statement balance. That means that having a large balance will drag down your ratio, regardless of whether or not you’re on track to pay it down. The tool breaks out all your debts by category so you can visualize how small amounts can gobble up your income.

Once your back-end ratio reaches forty-three percent, you’ve reached the legal limit, which is called Qualified Mortgage rule. At this stage, most conventional lenders won’t approve your loan. There are exceptions. FHA may go as high as 50 percent, but only with some strong offsetting factors like excellent credit or significant savings.

In many cases, paying down your debt is less expensive than earning more money. To earn an extra $10,000 of gross income, you’ll need to bring home much more. Post-tax earnings. Wiping out a $200 monthly credit card bill reduces your DTI immediately and directly. It eases the pressure without having to await a pay increase.

You can easily plug various debt repayment plans into the calculator and see how they affect your finances. It’s not about numbers; it’s about strategy. Don’t sweat your debt-to-income ratio (DTI). It’s just a snapshot of how much breathing room you have today. It doesn’t reflect what you did in the past or how hard you work, it reflects whether you earn enough to pay your bills; including a new mortgage payment, every month.

A high number isn’t a death sentence; it’s just an indicator to cut back your spending. Refinance high-interest debts, pay off your revolving accounts or give yourself time to pay down a short-term debt. Strive for sustainability. Don’t strive for perfection. When you go to the closing table, you want to know you’ll still have money left over after the second month of homeownership. Keep low ratios and listen to the numbers speak before signing on the dotted line. It’s naturaly important to check your financals.