Rental Property Depreciation Calculator

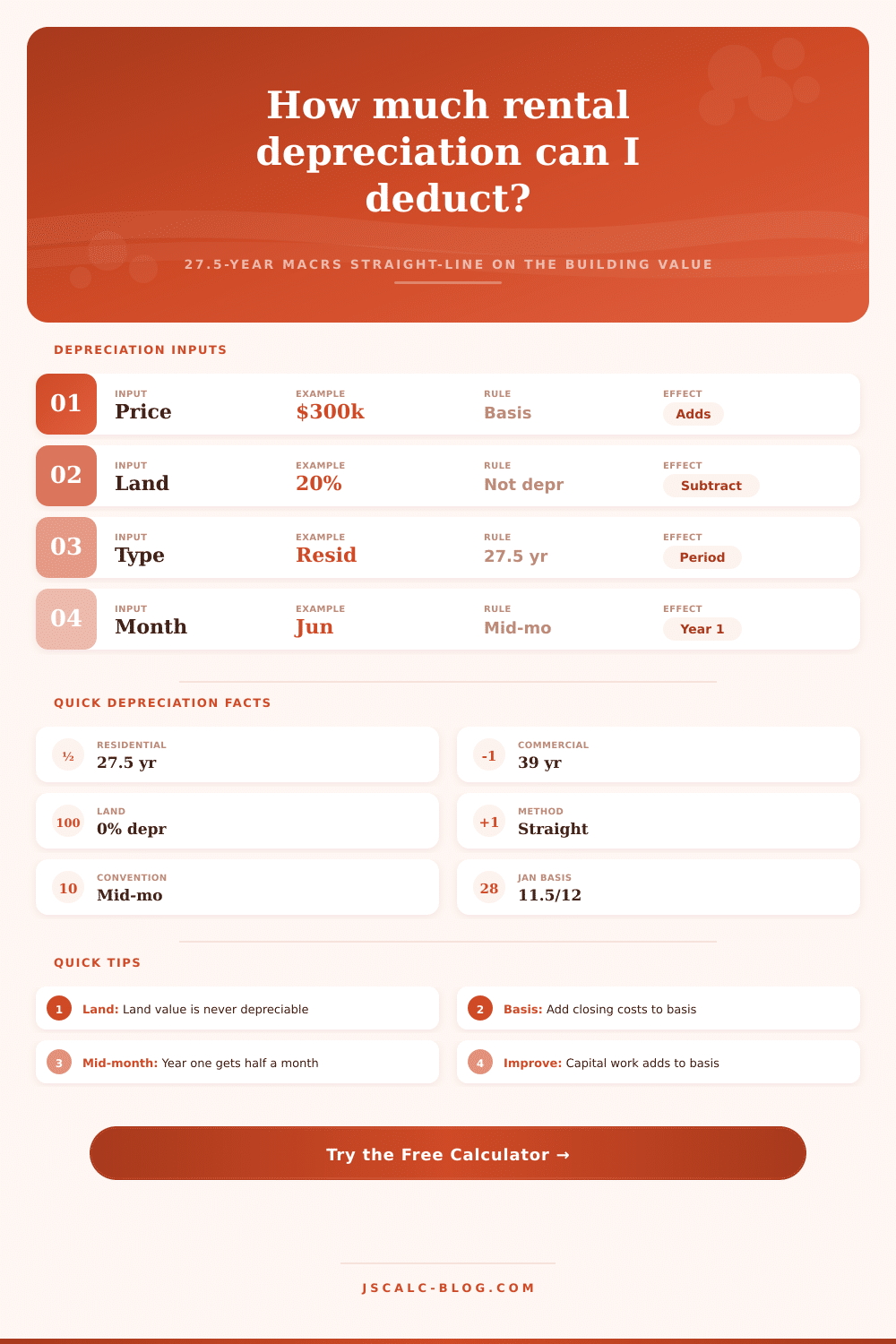

Estimate your annual straight-line depreciation deduction on a U.S. residential rental using the 27.5-year MACRS recovery period, the mid-month convention, and a full year-by-year schedule. Land is excluded because only the building is depreciable.

🎯Real Property Presets

📝Property & Basis Inputs

Total price paid for land plus building.

Land is not depreciable. Used when method is percent.

Used when method is dollar amount.

Title, legal, transfer tax, survey, recording.

New roof, HVAC, addition, and similar work.

Mid-month convention applies to the first year.

Used for total depreciation to date.

Estimates the yearly tax savings from the deduction.

🔢Method Snapshot

📊Year-by-Year Depreciation Schedule

| Tax Year | Calendar Year | Deduction | Accumulated | Remaining Basis |

|---|---|---|---|---|

| Enter values above to build the depreciation schedule. | ||||

📆First-Year Mid-Month Convention Table

| Placed In Service | Months Counted | Year-1 Fraction | % of Full Year | On Your Basis |

|---|---|---|---|---|

| The mid-month table appears after calculation. | ||||

The month placed in service is treated as if it were placed at the midpoint of that month, so the first year receives half a month of depreciation for that month plus each later month in the year.

🗂Residential vs Commercial Reference

| Asset Class | Recovery Period | Method | Convention | Annual Rate |

|---|---|---|---|---|

| Residential rental building | 27.5 years | Straight-line (GDS) | Mid-month | 3.636% |

| Commercial / nonresidential | 39 years | Straight-line (GDS) | Mid-month | 2.564% |

| Residential under ADS | 30 years | Straight-line (ADS) | Mid-month | 3.333% |

| Land | Not depreciable | None | None | 0% |

| Land improvements (fence, drive) | 15 years | 150% declining | Half-year | Varies |

| Appliances / carpet (5-yr) | 5 years | 200% declining | Half-year | Varies |

💰Land Allocation Comparison Grid

| Land Share | Land Value | Building Basis | Annual Deduction | 10-Year Total | Tax Saved / Yr |

|---|---|---|---|---|---|

| The land allocation grid appears after calculation. | |||||

Higher land allocation lowers the depreciable building basis, so the deductible amount shrinks. Assessor ratios often guide the split between land and improvements.

⚙Full Formula Breakdown

📋Reference Values

| Item | Typical Entry | How It Is Used | Effect On Deduction |

|---|---|---|---|

| Land share | 15% to 30% of price | Removed from basis | Higher land lowers deduction |

| Closing costs | 2% to 5% of price | Added to basis | Raises the yearly deduction |

| Capital improvements | $0 to $80,000+ | Added to basis | Raises depreciable amount |

| Recovery period | 27.5 or 39 years | Divides the basis | Longer period, smaller amount |

| Placed-in-service month | January to December | Sets year-1 fraction | Later month, smaller year one |

💡Practical Depreciation Tips

The numbers worked. Rent = Mortgage. There is leftover cash flow. Equity grows over time in the market. That’s the spiel. But what most novice landlords don’t think about until tax time rolls around is that there’s a silent partner in this formula. It is called depreciation. And he exist for one reason: the IRS knows that your building is gradualy declining into disrepair. They acknowledge that by giving you a statutory allowance that lets you deduct that loss, year after year. (In other words, you’re showing a paper loss on your taxes but still pocketing positive cash flow.)

The calculator up top take care of the number-crunching when you input your land value and purchase price. You won’t have to guess or wrestle with spreadsheets anymore. Remember this: Land doesn’t depreciate. The dirt doesn’t age. It just sits there. Therefore, when you purchase a $300,000 home, you can’t write off 100 percent of that price. You must divide that cost between the part you own (the structure) and the part you do not own (the land). Your deduction applies only to the structure.

Understanding Depreciation for Landlords

A lot of investors use the county assessor’s ratio for this split but it tends to be out-of-date. If you’re aware that house prices remained flat in your area, while land values skyrocketed, then you may want to use an old percentage because it will allow you to deduct too much depreciation. This becomes problematic down the line as you’ll end up owing depreciation recapture taxes when you sell. Play it safe and err on the side of caution. Keep your records justifiable.

For residential properties, the IRS allows you to spread building expense over twenty-seven point five years once you’ve isolated the cost of construction. Your annual deduction are equal to the depreciable basis divided by that amount. If you made any improvements when you owned the property (e.g., installed a central air system, put on a new roof), these aren’t deducted immediately; they’re simply added to the basis. This stretches out the benefit while keeping your deductions accurate. A nice reference table on page breaks it all down. There is also a separate table for commercial assets which have a longer period of thirty-nine years.

One other note: There’s a weird timing thing. Depreciation follows what the IRS calls the “mid-month” convention. So if you purchase the house in June, that means you’re not entitled to 12 months’ worth of depreciation that year. You’ll get half a month for June (huh?) and then the remaining portion of the year. It seems like a tiny penalty but it’s nice because everyone does it that way. This way they all play by the same rulebook. The tool produce a complete schedule explaining how the proration impacts your first year and how the last year compensates for the difference. You’ll notice that the deduction holds pretty steady throughout the midpoint years making it easier to plan finances around.

So what does this mean, aside from the short term tax bill? The answer: Depreciation lowers your taxable income while never costing you a dime. For most people, it makes a money-making investment into a paper losing position. If you’re lucky enough to have other income to shelter that’s where that protection comes in handy. But here’s the catch, for each dollar of depreciation, you’re lowering your basis in the property. Eventually, when you do sell, you’ll be required to pay recapture tax on the amount of depreciation you took out. It’s not a free lunch. It’s a loan from the Government for which you’ll should of repay with future gains.

Once you understand that trade-off, the way you think about the asset shifts. You’re no longer purchasing a house; you’re also managing a diminishing tax asset and an appreciating asset. Landlords are typically obsessed with their rental cash flow. Plus, of course, their mortgage payments. What they overlook is the silent loss in value taking place behind the scenes. This calculator tells you what that secret write-down amounts to. Run your personal numbers through it. You’ll see exactly how much money you’ve got left and how many more years of write-offs will exist. Suddenly, a vague idea becomes a real number you can count on each year.

But wait, take a minute to check your land allocation. Do any of those recent repairs counts as capital improvements? Run the numbers. Maybe you’re in for a surprise: Your property is being a quiet supporter, year after year. Give that silent partner some credit. Now you know just what’s owed to you.