Real Estate ROI Calculator

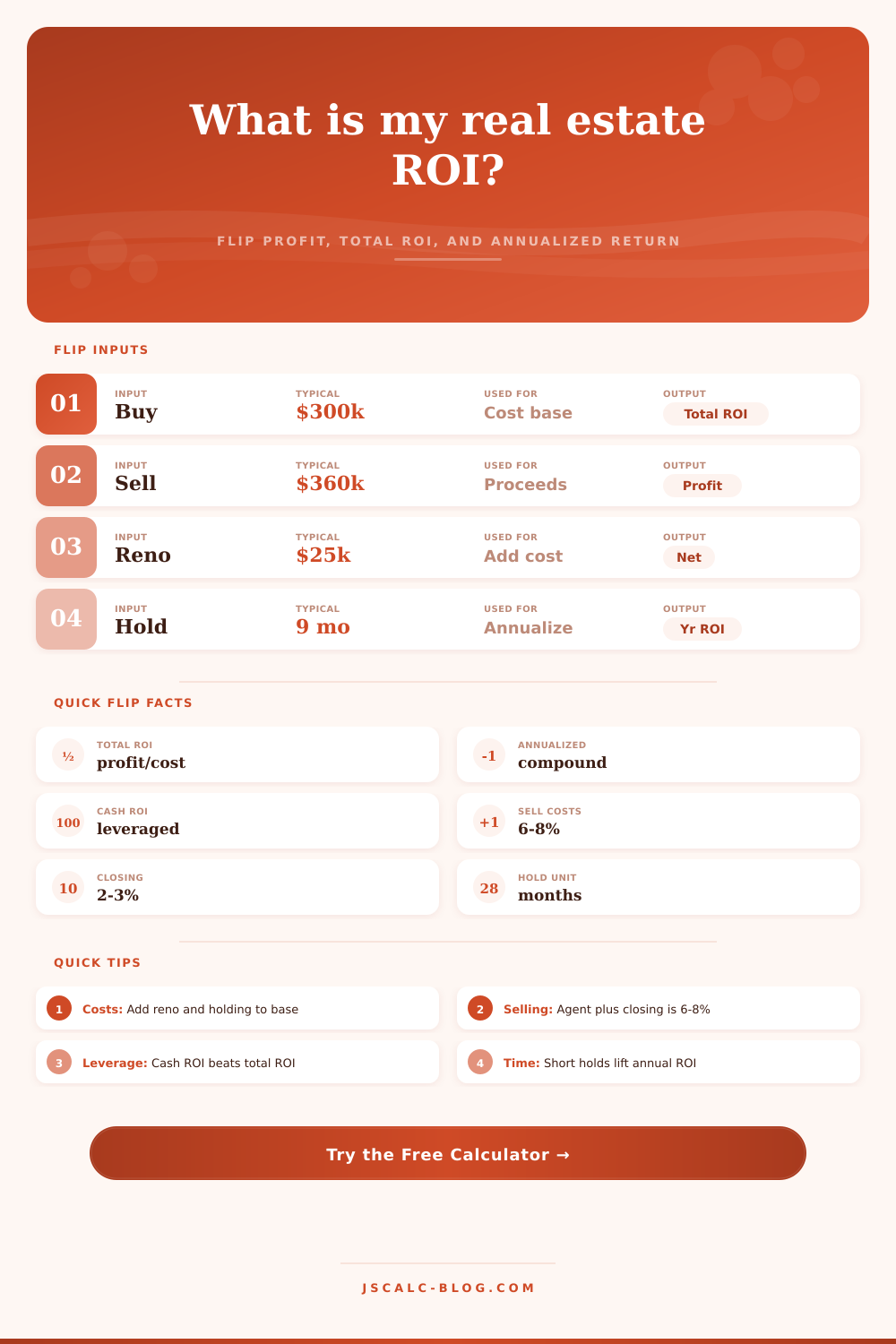

Model a buy-sell or fix-and-flip deal from purchase to closing. Enter your price, costs, renovation, holding, and resale numbers to see total ROI, net profit, annualized return, and leveraged cash-on-cash ROI.

🎯Real Flip & Resale Presets

📝Deal Inputs

Title, escrow, lender, and inspection fees at buy.

Taxes, insurance, utilities, and loan interest while held.

Applied to sale price. Agent commission plus seller closing.

Used for cash-on-cash ROI when financed.

🔢Formula Snapshot

📊Cost & Profit Breakdown

| Line Item | Category | Amount | Share of Cost | Notes |

|---|---|---|---|---|

| Enter your deal above to build the cost and profit breakdown. | ||||

🗓ROI vs Annualized by Hold Time

| Hold Period | Months | Total ROI | Annualized ROI | Profit / Month |

|---|---|---|---|---|

| The annualized reference appears after calculation. | ||||

⚖Flip vs Hold Comparison

| Strategy | Exit Timing | ROI Driver | Total ROI | Annualized |

|---|---|---|---|---|

| The flip versus longer-hold comparison appears after calculation. | ||||

🗂Selling-Cost Reference & Deal Grid

| Scenario | Buy | Sell | Reno | Sell % | Hold | Total ROI |

|---|---|---|---|---|---|---|

| Fix & Flip | $275k | $360k | $32k | 7.0% | 8 mo | ~11% |

| Quick Flip 6mo | $240k | $285k | $18k | 6.0% | 6 mo | ~5% |

| All-Cash Flip | $180k | $245k | $28k | 7.0% | 7 mo | ~11% |

| Financed 20% Down | $320k | $400k | $35k | 7.5% | 10 mo | ~4% |

| Renovation Add-Value | $260k | $375k | $55k | 7.0% | 11 mo | ~11% |

| Appreciation Play | $400k | $470k | $8k | 6.5% | 18 mo | ~6% |

| 12-Month Hold | $350k | $420k | $22k | 7.0% | 12 mo | ~5% |

| Break-Even | $300k | $333k | $8k | 7.0% | 9 mo | ~0% |

⚙Full Formula Breakdown

📋Selling-Cost Reference

| Cost Item | Typical Range | Applied To | Effect on ROI |

|---|---|---|---|

| Agent commission | 4.5% to 6.0% | Sale price | Largest drag on net proceeds |

| Seller closing | 1.0% to 2.0% | Sale price | Title, escrow, transfer taxes |

| Purchase closing | 2.0% to 3.0% | Purchase price | Raises the total cost basis |

| Renovation | Project based | Total cost | Should lift resale by more than spend |

| Holding costs | Rises with time | Total cost | Longer holds cut annualized ROI |

💡Practical Flip ROI Tips

Here’s the deal: you come across a house that appears to be a project. At a quick glance, you do some quick mental math on the curb and it feel like a winner. The price is low enough. It has high enough potential. There is a wide enough gap between the buy and sell prices to cover your risk.

But here’s the thing about flipping houses. It’s not just about the spread. What happens in the middle is everything. That six month renovation window is where money bleeds out of your pocket every single day, that’s where deals go to die.

How to Calculate Real Profit in House Flipping

This is where the calculator above do all the heavy lifting. It takes those vague gut feelings and turns them into hard numbers in terms of annualized yield and total return. Everyone sees $30,000 and says “I made such a good investment.” No one thinks about time. $30,000 earned in six months is far more valuable then $30,000 earned over two years.

The math reflects this with its total return based off how long you hold it. Every week that it sits stale on the market and every week it delay construction is reflected in the final total return number. That total return number looks fine until you see the annualized rate collapse under those mounting taxes and interest. It’s an easy adjustment, just makes you view every week like a leveraged piece of your own capital.

And finally, there’s the question of cost vs. This refers to cash. If you buy with a loan, then your big investment will include not only the purchase price but also the repair costs. However, the cash you’ll write checks for could be significently less than that.

This distinction is important: it creates two different definitions of success. Success #1 defines profit as a percentage of your overall project cost. Success #2 defines profit as a percentage of the actual cash you withdrew from your bank account. Focus solely on the latter number, and leverage can make a mediocre deal look fantastic. Focus on the former, and you realize that you’re adding to your holding costs by paying interest on money you borrowed.

To determine whether you’re really creating wealth, you have to look at both numbers. It makes you deal with the sunk costs that tend to be hidden by vague estimations. Closing costs alone can suck two-three percent off the top of purchase price immediately. Those aren’t discretionary line items. That’s gravity. They’ll rob from your last paycheck if you don’t include them in starting formula.

You can adjust those cost figures to reflect reality in your local markets. Transfer taxes may be nominal in certain places. In others, it’s a meaningful drag against net proceeds. Failing to acknowledge the difference is a path to dissapears at the closing table.

Optimism always trumps realism when it comes to renovation budgets. Based on the stuff you read online, you estimate that it’ll cost you twenty grand to remodel the kitchen. You open a cabinet and discovers mold under the drywall or outdated wiring. The closer your estimates become to solid numbers, the more you can adjust this renovation figure up or down with the calculator.

It is better to be safe at the start rather than find out too late that unexpected repairs have eaten up your profit margin. This isn’t about predicting the future. This is about creating a buffer to keep you from going broke when things inevitably go wrong.

So in summary, this isn’t some magic number tool; it’s more of a way to stress test your assumptions. How sensitive is the deal to cost fluctuations or timeline delays? What happens when the sale price decreases five percent? Do you still make money? What happens when the hold costs increase one thousand dollars per month? Does the math still work?

This allows you to take the emotion out of the process before signing any contracts. Instead of being hopeful for the best case scenario, you can prepare yourself for the most likely one. And that mental switch is what distinguishes amateurs (who get killed during bad markets) versus professionals (who thrive during bad markets).

The math doesn’t lie. But the math will only tell you the truth if you’re honest with the numbers you input into it. You should of known that.