Property Tax Calculator

Estimate annual and monthly property tax from home market value, assessment ratio, homestead and senior exemptions, and either an effective tax rate or a local mill rate. Includes state reference rates and a full formula breakdown.

🎯Real Property Tax Presets

📝Property Details

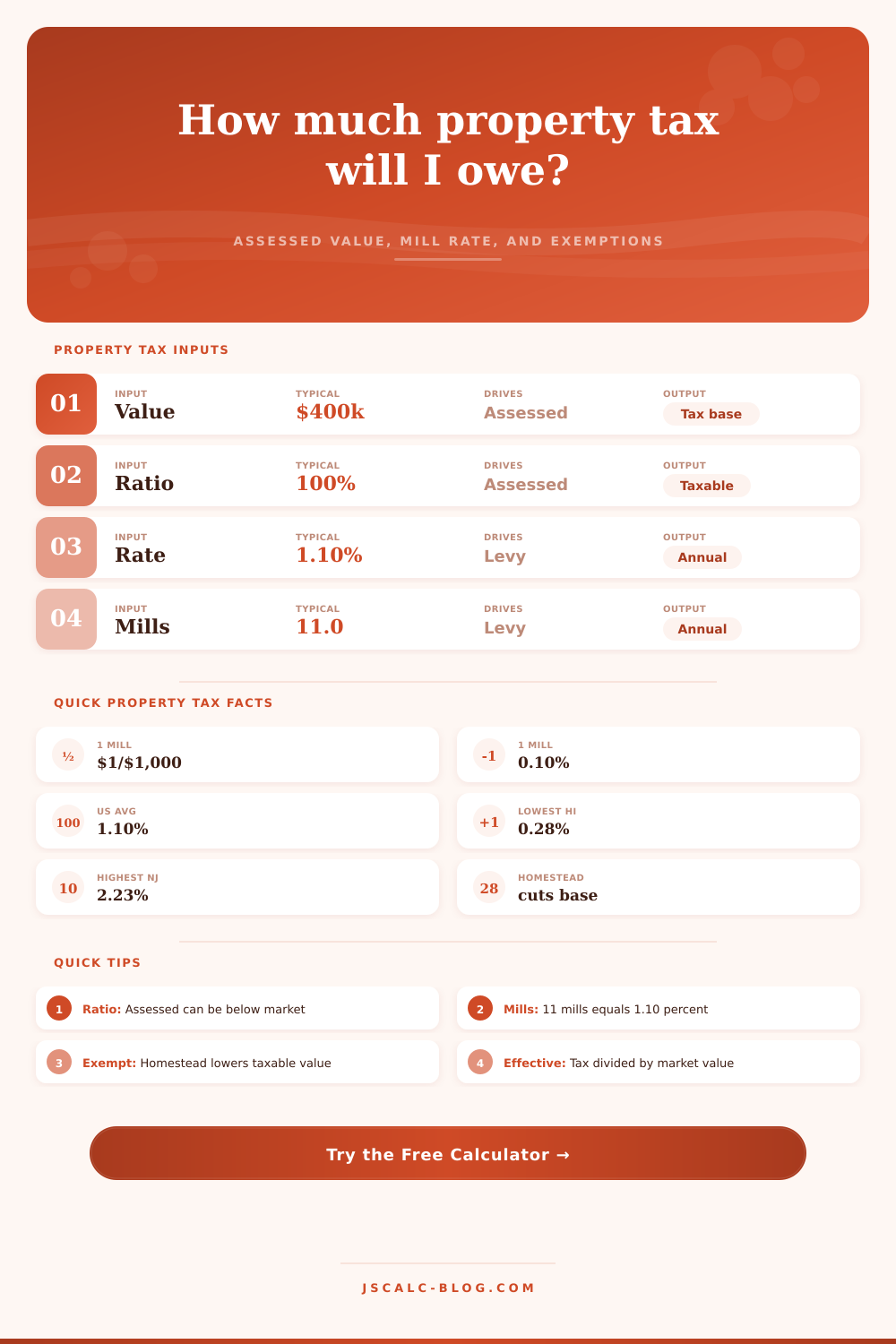

Many counties assess at 100%; some use a lower fractional ratio.

Used when mode is effective tax rate.

Used when mode is mill rate. 11 mills = 1.10%.

🔢Formula Snapshot

📊State Effective Property Tax Rates

| State | Effective Rate | Approx Mills | Tax on $400k |

|---|---|---|---|

| New Jersey | 2.23% | 22.3 | $8,920 |

| Illinois | 2.08% | 20.8 | $8,320 |

| New Hampshire | 1.93% | 19.3 | $7,720 |

| Connecticut | 1.79% | 17.9 | $7,160 |

| Texas | 1.68% | 16.8 | $6,720 |

| New York | 1.40% | 14.0 | $5,600 |

| US Average | 1.10% | 11.0 | $4,400 |

| Florida | 0.86% | 8.6 | $3,440 |

| California | 0.71% | 7.1 | $2,840 |

| Colorado | 0.51% | 5.1 | $2,040 |

| Hawaii | 0.28% | 2.8 | $1,120 |

🔁Mill Rate to Percent Reference

| Mill Rate | As Percent | Per $1,000 | On $250k Taxable |

|---|---|---|---|

| 5 mills | 0.50% | $5.00 | $1,250 |

| 10 mills | 1.00% | $10.00 | $2,500 |

| 15 mills | 1.50% | $15.00 | $3,750 |

| 20 mills | 2.00% | $20.00 | $5,000 |

| 25 mills | 2.50% | $25.00 | $6,250 |

| 30 mills | 3.00% | $30.00 | $7,500 |

📐Assessment Ratio Examples

| Assessment Ratio | Market Value | Assessed Value | Note |

|---|---|---|---|

| 100% | $400,000 | $400,000 | Full market assessment |

| 80% | $400,000 | $320,000 | Fractional local ratio |

| 50% | $400,000 | $200,000 | Half-value assessment |

| 40% | $400,000 | $160,000 | Low fractional ratio |

| 33% | $400,000 | $132,000 | One-third assessment |

| 10% | $400,000 | $40,000 | Very low ratio class |

🗂Exemption Type Comparison Grid

| Exemption Type | Typical Amount | Who Qualifies | Applied To | Renewal | Tax Effect |

|---|---|---|---|---|---|

| Homestead | $25k to $50k | Primary residence owner | Assessed value | Often one-time | Lowers taxable base |

| Senior citizen | $10k to $65k | Age 65+ with income limits | Assessed value | Annual or periodic | Extra base reduction |

| Disabled veteran | Up to 100% | Service-connected disability | Assessed value | Verify status | May fully exempt |

| Disability | $10k to $25k | Documented disability | Assessed value | Annual proof | Reduces taxable base |

| Widow / widower | $5k to $10k | Surviving spouse | Assessed value | Varies by state | Small base reduction |

| Agricultural | Use-value basis | Qualifying farmland | Assessment method | Annual filing | Assessed at use value |

| Circuit breaker | Income based | Low-income owners | Tax bill / credit | Annual filing | Caps tax vs income |

⚙Full Formula Breakdown

📋Reference Values

| Item | Common Entry | How It Is Used | Effect On Tax |

|---|---|---|---|

| Market value | $150k to $900k | Base for assessed value | Scales the whole bill |

| Assessment ratio | 10% to 100% | Value × ratio / 100 | Lower ratio, lower base |

| Effective rate | 0.28% to 2.23% | Taxable × rate / 100 | Sets the levy directly |

| Mill rate | 2.8 to 22.3 mills | Taxable × mills / 1000 | 10 mills equals 1.00% |

| Exemptions | $0 to $65k each | Subtracted from assessed | Cuts taxable value |

💡Practical Property Tax Tips

The four hundred thousand dollar house (that’s the big ticket). You’ve celebrated milestone of buying your house, but then you look up and suddenly realize you have no idea what it costs to maintain.

You signed the deed, got the keys, but now it’s time to pay local government their share. Property taxes aren’t just a line item in your budget: they’re typically one of the biggest recurring expenses associated with owning a home (second only to mortgage payment). Most homebuyers get fixated on purchase price and treat property taxes like an afterthought … until first statement shows up in the mail.

Understanding Property Taxes for Homeowners

Once you plug in your unique details, the calculator above will do the rest for you so you don’t have to guess at how local rates converts into real-world dollars. Before you calculate tax, though, you first need to understand what you’re actualy calculating the tax for.

The market value of your home is just that: the market value of your home. That might not be exact dollar figure used by the county. Rather than using the market value as-is, counties will take the market value and then multiply it by an “assessment ratio.” Depending on where you live, that ratio could be 100%, which would mean your assessed value would equal actual (on-paper) value of your home. But in other locations, the ratio may be 50%, maybe even less!

That fraction sounds arbitrary, but it helps even out the valuation of various property types against a wide range of other properties within that same tax base. Unless you know what ratio your county applys, your guess is as good as… well, whatever.

Next, we have the “mill rate,” which is one dollar per $1,000 worth of property (taxable) value, hence the term ‘mill,’ as in ‘one thousand.’ You can easily turn this number into a percentage by just shifting decimal over a spot: 11 mills = one point one percent effective rate. The rate chart on the page shows how much your city or county might charge you compared to other states, like Hawaii’s low taxes versus New Jersey’s high taxes.

That’s why, instead of just depending on state income tax, these taxes gets used to pay for things like roads, schools and emergency services from local government. If you don’t want to move, the quickest way to reduce your tax bill is through exemptions.

By filing for a homestead exemption, you’ll knock a flat dollar amount off your property’s value (typically tens of thousands), which is taxed at same rate as the rest of it. Likewise, if you’re a veteran or senior, you may be able to get an exemption that lowers the value before the rate applies. Unlike the deductions, where the IRS will check whether you still meet the criteria each year; a homestead exemption gives you savings forever, on an annual basis.

Most people neglect to request this benefit because they assume the government would of known if they’ve taken up residency somewhere. They don’t. Prove you live there, or prove you’re a vet/senior/etc., then go apply. This tiny bit of paperwork could save you hundreds, if not thousands, over the next 10+ years.

There’s also effective rate, which shows what portion of the price of your house you’re actualy paying, as a percentage of its market value. You get it by dividing the tax (minus exemptions) by initial market value. Because we’ve narrowed down the base, the effective rate is usually lower than the stated mill rate seem to be.

That’s why it’s important when you’re trying to compare prices among different cities/neighborhoods. A city with an overall higher mill rate may have lower effective rates because they assess generously. Likewise, a city with lower mill rates but higher valuations may has higher actual dollar amounts on their bills.

To get a sense of what this will do to your cash flow (i.e., to budget accordingly), don’t just look at it as an annual number. Property taxes are usually included in your mortgage; that’s known as an “escrow” account and it spreads out the lump sum to something more manageable. You can adjust the view from monthly to annual, quarterly or semi-annual. That way, whatever loan structure you have, you know exactly how much you’re paying each period, and you won’t be surprised by a budget shock when you recieve a renewal notice in the mail.

Your property tax is variable, because the budget changes locally and because of reassessment. Watch how it’s trending in your county so you know when the hike come due (before it arrives on your statement). Learn what makes up your bill so you have the power to check for mistakes…or challenge one that’s not fair. Turn it from a confusing government assessment into something clear and useful that you can plan around.

You’re the owner of this house, yes. But you also now own the responsibility to understand what holds it upright both financially and legaly.