Mortgage Refinance Calculator

Compare your current mortgage against a new refinanced loan to see the monthly savings, how many months it takes to earn back closing costs, and the lifetime interest difference over both payoff schedules.

🎯Real Refinance Scenarios

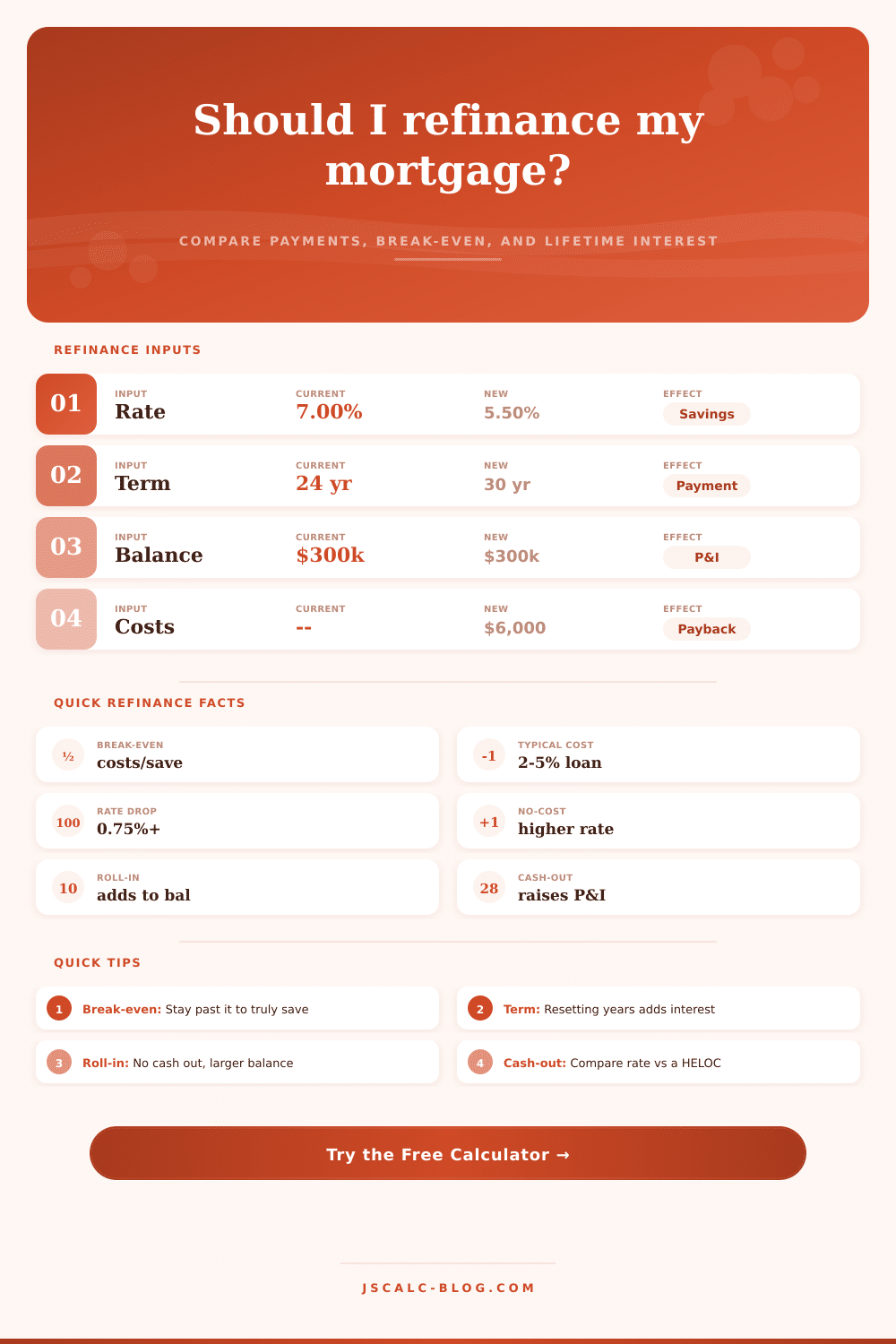

📄Current Loan

The payoff amount you still owe today.

Years left on the current loan by default.

🆕New Refinanced Loan

Lender, title, appraisal, and recording fees.

Extra cash added to the new balance.

🔢Formula Snapshot

⚖Current vs New Side by Side

| Measure | Current Loan | New Loan | Difference |

|---|---|---|---|

| Enter values above to compare the two loans. | |||

📈Break-Even by Year

| Year | Cumulative Savings | Closing Costs | Net Position | Status |

|---|---|---|---|---|

| The break-even progression appears after calculation. | ||||

📊Rate vs Savings Sensitivity

| New Rate | New Payment | Monthly Savings | Break-Even |

|---|---|---|---|

| The sensitivity grid appears after calculation. | |||

🗂Refinance Scenario Grid

| Scenario | Balance | Rate Change | New Term | Closing Costs | Best When |

|---|---|---|---|---|---|

| Rate drop 30yr | $300k | 7.00% → 5.50% | 30 yr | $6,000 | Staying long term |

| Shorten to 15yr | $300k | 7.00% → 5.25% | 15 yr | $6,500 | Kill interest fast |

| Cash-out $40k | $260k | 6.75% → 6.25% | 30 yr | $7,500 | Fund a project |

| Same term refi | $275k | 6.90% → 5.90% | 25 yr | $5,500 | Keep payoff date |

| No-cost refi | $250k | 7.10% → 6.10% | 30 yr | $0 rolled | Short stay ahead |

| Jumbo refi | $720k | 7.25% → 6.10% | 30 yr | $12,000 | Large balance |

📋Typical Closing-Cost Components

| Component | Typical Range | What It Covers | Notes |

|---|---|---|---|

| Loan origination | 0.5% to 1.5% | Lender processing fee | Sometimes negotiable |

| Appraisal | $400 to $700 | Home value estimate | May be waived |

| Title & escrow | $700 to $2,000 | Title search and insurance | Varies by state |

| Credit & underwriting | $300 to $900 | Credit pull and review | Bundled by some lenders |

| Recording & transfer | $50 to $500 | County filing fees | Set by local government |

| Discount points | 1% per point | Buys down the rate | Optional prepaid interest |

⚙Full Formula Breakdown

💡Practical Refinance Tips

You’ll seldom see mortgage refinance math reduced to such simplicity: Your closing costs divided by your monthly savings = Done! That’s your break-even point, fine! But what about the human factor? How many years do you plan to livig in this house, anyhow?

A lot of folks focus on their new lower monthly payment and think they’ve come out ahead. They might not realize they could end up paying far more interest over life of loan by resetting clock on 30-year mortgage, when they could have simply held onto there existing rate.

How to Decide if Refinancing is Right for You

To use it: Before you believe its output, however, know what’s feeding in. Every dollar you owe will be subject to your new rate. This means the outstanding balance is where anchor lies, as all of the dollars you owe accrues interest on the new rate. All of that additional cash you’re removing from your pocket (whether consolidating debt or doing renovations) gets rolled into principal and increases your payment, even if rate goes down a bit. This is a give-and-take, paying now vs. It costs more later.

To see how rolling those expense into the loan would impact your bottom line, you don’t have to grab a spreadsheet, calculator does that math for you. Most decisions depend on break-even timeline. If it takes thirty months to earn back your closing costs, such as six thousand dollars, will you still be in home long enough to recoup them? For example, if it takes thirty months to earn back those six thousand dollars in closing costs, does that fit with how long you plan to stay?

Well, if you intend to sell within two years, then you’ve basically given a gift to the bank. Sure, you’ll save money on interest, but you’ll never make up for fees. But what if you treat this as your primary residence, and you’re going to live there for 20 years? In that case, upfront costs are meaningless against long-term savings.

That’s why the test shows the math: How much does a half percent difference affect your break-even point? When you have a large loan amount, even tiny differences compounds fast and justify the cost in the long run. The other trap is psychological aspect of lowering the payment versus lengthening the term. Lowering your rate and increasing the mortgage length back out to 30 years looks good in monthly budget, but bad in net worth column. The same pile of interest gets stretched out across additional months, lessening the pain but multiplying the volume. Bringing down the term from 30 years to 15 years will usually result in a higher payment then you had before, but destroys interest at a pace that no rate drop can match. That’s why headline monthly number isn’t as important as lifetime difference in interest.

There’s also another thing about closing costs that should of been looked at: They’re not fixed. In fact, lenders frequently throw around “no-cost” refinancing deals in which they swallow the fees but charge a bit more interest in return. Fine, if you intend to sell shortly (you’ll save yourself the immediate cash outlay, and won’t have time to spread out the cost of the higher rate and lose money). Otherwise, it’s generaly better to pay points up-front to buy down your rate; especially if you intend to hold. It all depends on your horizon.

Your credit health is the quiet hero in all of this. If it’s pristine you get the rates they advertise; if it isn’t you’ll get spread out wider (or pay more discount points) to wipe away what you’d thought was a good deal. Check your credit report far in advance of rate shopping, fixing errors requires time, which a speedy refi may not allow.

To illustrate this, here’s a handy calculator (above) that can help you see side-by-side how much you’re paying now vs. What you’d pay if you refinanced: Play around with various cost parameters and length-of-stay scenarios. It’s not about reducing your payment by any means necessary. It’s about making your debt work better. If you determine the optimal tradeoff between short-term cashflow relief and future savings, then you have a no-brainer answer: You’ll refinance. Refinancing isn’t an “event”; it’s a financial tool. Approach it like any large financial decision: Listen to the numbers, not the hype.