Compound Interest Calculator

Project a starting balance, recurring deposits, compounding frequency, APY, interest earned, after-tax estimate, and inflation-adjusted spending power from one focused worksheet.

Deposits are modeled with an effective rate per deposit period so weekly, monthly, quarterly, and annual contributions stay aligned with the selected compounding schedule.

A = P(1 + r/n)^(nt)

P is the starting principal, r is APR as a decimal, n is compound periods per year, and t is years.

FV = PMT * (((1 + i)^m - 1) / i)

PMT is the deposit amount, i is the effective rate per deposit period, and m is total deposits. Beginning-period deposits are multiplied by (1 + i).

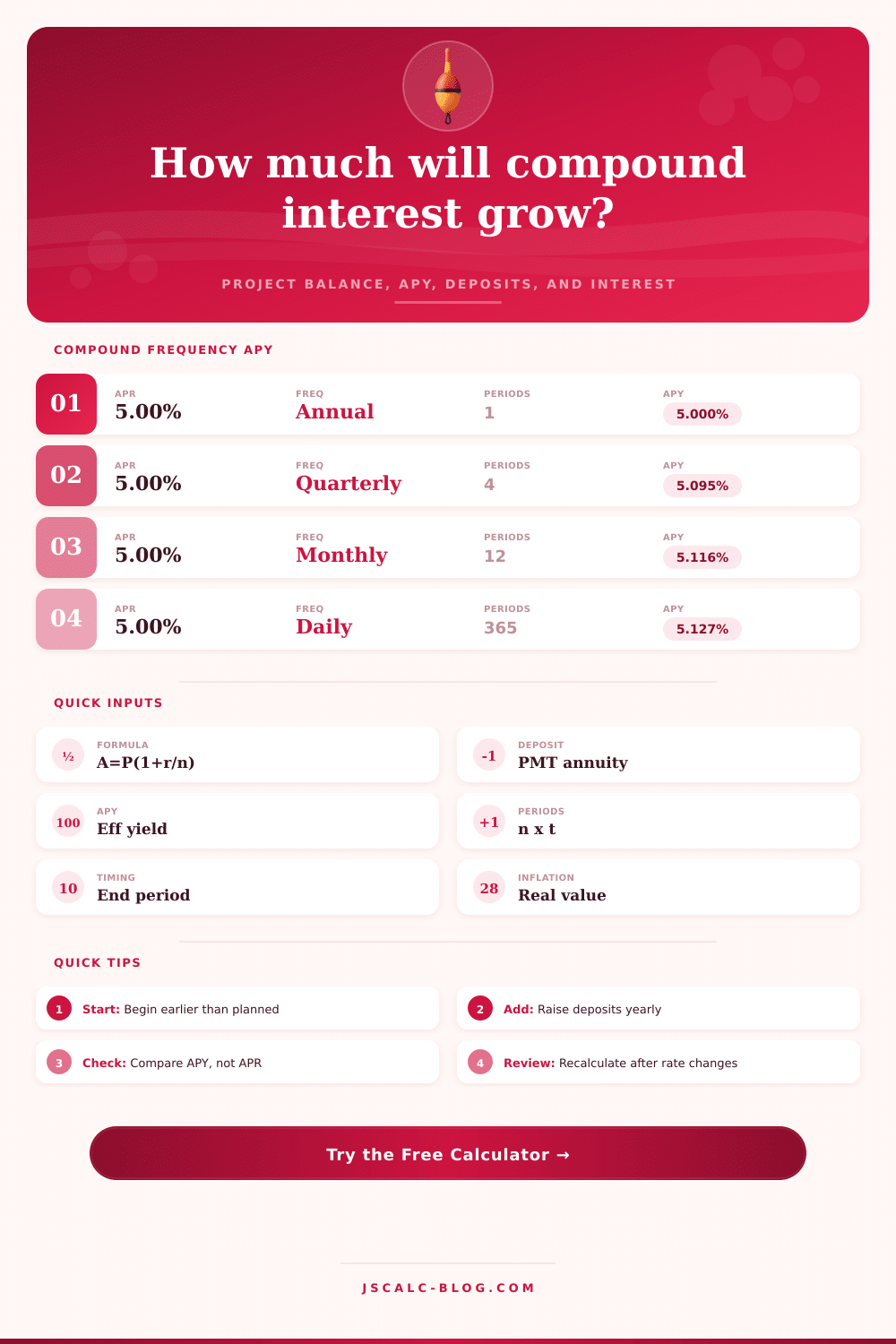

APY = (1 + APR/n)^n - 1

APY converts the stated APR and compounding schedule into the effective one-year yield before new deposits.

| APR | Compounding | Periods per year | Periodic rate | APY |

|---|---|---|---|---|

| 5.00% | Annual | 1 | 5.0000% | 5.000% |

| 5.00% | Semiannual | 2 | 2.5000% | 5.063% |

| 5.00% | Quarterly | 4 | 1.2500% | 5.095% |

| 5.00% | Monthly | 12 | 0.4167% | 5.116% |

| 5.00% | Weekly | 52 | 0.0962% | 5.125% |

| 5.00% | Daily | 365 | 0.0137% | 5.127% |

| Scenario | APR | Monthly deposit | Years | Final balance | Interest earned |

|---|---|---|---|---|---|

| Cash reserve | 3.00% | $250 | 5 | $28,284 | $3,284 |

| Short goal | 4.00% | $300 | 8 | $44,678 | $5,878 |

| Balanced path | 5.50% | $400 | 12 | $92,041 | $24,441 |

| Index habit | 7.00% | $500 | 20 | $306,725 | $176,725 |

| Growth saver | 8.00% | $650 | 25 | $695,240 | $490,240 |

| Catch-up plan | 7.00% | $1,000 | 15 | $341,748 | $151,748 |

| Long horizon | 6.50% | $300 | 30 | $402,216 | $284,216 |

| Heavy saver | 7.50% | $1,500 | 20 | $863,347 | $493,347 |

| Deposit pattern | Assumptions | Total deposited | End-period FV | Beginning FV |

|---|---|---|---|---|

| $100 monthly | 5% APR, 10 yrs | $12,000 | $15,528 | $15,593 |

| $250 monthly | 6% APR, 20 yrs | $60,000 | $115,510 | $116,088 |

| $500 monthly | 7% APR, 30 yrs | $180,000 | $609,985 | $613,543 |

| $1,000 monthly | 8% APR, 15 yrs | $180,000 | $346,039 | $348,346 |

| Annual return | Approx double time | Exact annual compounding | Use case |

|---|---|---|---|

| 3% | 24.0 years | 23.45 years | Cash-like growth |

| 5% | 14.4 years | 14.21 years | Moderate yield |

| 7% | 10.3 years | 10.24 years | Long-term mix |

| 9% | 8.0 years | 8.04 years | Growth tilt |

| 12% | 6.0 years | 6.12 years | High volatility |

We all know saving money makes money grow. Understanding how fast, and what makes it go faster. Is where most of the trick lie. It is not the number on interest rate label, but the mechanics of compounding, along with time and consistency.

Compound interest was supposedly called by Albert Einstein the eighth wonder of the world, which sounds like hyperbole until you see your own balance sheet over two decades. Then it begin to feel less magical then simply physical. Gravity behaves different in finance.

Why Compound Interest Matters

The tool above will do the math for you, but the way you think about what goes into the tool matter. Normally people begin by putting their principal in: the amount of money they have now. Fair enough. That’s the cash on hand. For most of us, though, the true engine isnt the initial lump sum. The true engine are the recurring deposit.

Consider your own budget. Saving an extra two hundred dollars a month versus three hundred don’t look like much on paper. But over the course of two decades at a seven percent return, an extra hundred bucks a month add up to almost sixty thousand more in ultimate value. It is not a rounding error. That’s the difference between retiring with a mortgage or without one.

The way interest rates are reported set up a sneaky trap. Banks like to brag about their APRs. Wall Street favors APY. Why does that matter? Because an APR assume no compounding of interest. An account that compounds monthly have a greater effective yield than its APR suggests. It’s laid out nicely in reference table on the page. Five percent APR compounded annually equals…five percent. Five percent compounded daily pushes to just over five point one percent.

That half of a percent don’t seem like much when you’re talking about a year. Thirty years later, it’s thousands of dollars. You don’t have to be a math whiz to understand the importance of seeking out best APY versus searching for highest APR.

People also overlook another variable: timing. When should your deposit go into the account, on the first of the month or the 15th? Who cares?) Both situations are covered by the calculator. But here’s the point: Cash in market for longer periods earns more. Cash deposited at start of period beats cash deposited at end because former has an additional period to compound. When your budget isnt flexible. When you’re squeezing all available growth out of a fixed sum. This make a difference.

Inflation is the invisible tax you pay now to yourself later. A million bucks… That’s a finish line! But what can that million buy in today’s world? Not much. It is worth seventy thousand dollars if you want things to be same twenty years from now. The tool helps you adjust for this. If you have one million dollars, the tool will take away amount that those dollars were inflated by.

This forces you to have an honest discussion with yourself about growth. Does your account grow because you’re inflating your bank balance? Or do you increase your buying power? When retirement comes, all that matter is your real returns, those are the ones that make you comfortabley.

Compound interest is something many think of as a set-it-and-forget-it deal. Partly yes. It’s better off on auto-pilot. But don’t ignore it completely. Things change. Rates adjust, and life happens. If you get a pay increase, recalculate. When rates go up, recalculate. Keep your plan in tune with reality.

The tool also has preset options for visualizing a variety of scenarios; from building an emergency fund to planning for retirement catch-up accounts. It reveals how difficult it is to play catchup if you start late, as you would of had to save a lot of money. Add more money? Yes. Add back years? No. Most people overlook this.

Begin with the end in mind. Begin with your current circumstances. Begin now. Don’t wait until you have the “perfect” amount. Patience is much better rewarded by the math than perfection is. Every single time, a modest plan begun early beats a grand plan begun late. Stick to being consistent and let the numbers do the heavy lifting. It’s an upward sloping line at first, but it’s vertical after that. You gotta stay in the game long enough to see the steep part.