Velocity Banking Calculator

Simulate the HELOC chunking strategy against your mortgage. See a new payoff date, total interest saved, and an honest side-by-side against simply applying the same monthly cash-flow surplus as extra principal.

🎯Real Velocity Scenarios

📝Mortgage & Cash Flow Inputs

All money that lands in your account each month.

In auto mode, exclude the mortgage; P&I is added for you.

Lump sum drawn from the HELOC each cycle.

Auto adds the amortized P&I on top of other expenses.

Set your known P&I payment, or leave 0 to auto-calculate.

🔢Strategy Snapshot

📊Standard vs Velocity vs Extra Pay

| Strategy | Payoff Time | Total Interest | Interest Saved | Time Saved | Extra Cost |

|---|---|---|---|---|---|

| Enter values above to compare the three payoff strategies. | |||||

🔁Chunk Cycle Timeline

| Cycle | Chunk Drawn | Balance After | Payback Months | HELOC Interest | Running Interest |

|---|---|---|---|---|---|

| The chunk-by-chunk timeline appears after calculation. | |||||

🗂Chunk Size Impact

| Chunk Size | Payback Months | HELOC Cost / Chunk | Est. Payoff | Interest Saved | Verdict |

|---|---|---|---|---|---|

| Chunk-size sensitivity appears after calculation. | |||||

📋Cash-Flow & Interest Reference

| Monthly Surplus | Chunk to Match | Payback Months | Rough Payoff | Typical Interest Saved | Notes |

|---|---|---|---|---|---|

| $300 | $3,000 or less | 10+ mo | Long | Small | Thin margin, high risk |

| $600 | $5,000 | 8 to 9 mo | Slowly faster | Modest | Watch the LOC rate |

| $1,000 | $8,000 | 8 mo | Faster | Meaningful | Common starting point |

| $1,500 | $10,000 | 7 mo | Much faster | Strong | Solid surplus zone |

| $2,500 | $15,000 | 6 mo | Very fast | Large | Extra pay rivals it |

| $3,500 | $20,000 | 6 mo | Aggressive | Largest | Just pay extra instead |

⚙Full Method Breakdown

💡Velocity Banking Tips

Sounds pretty clever right? This is called velocity banking, and it looks like an accountant’s head-spinning attempt at financial trickery. Here’s the basic concept: use a line of credit to repay your mortgage principal. Then, repay the line of credit with whatever excess cash flows into your bank account each month. It sounds like you’re paying off your mortgage faster by outsmarting yourself. It is financial engineering!

But here’s where things get complicated: It’s actualy a little more complex, and it relies on numbers… not magic. So will it help you? That depends completely on the size of your interest rate spread and your ability to stick to the repayment schedule.

Is Velocity Banking Really Worth It?

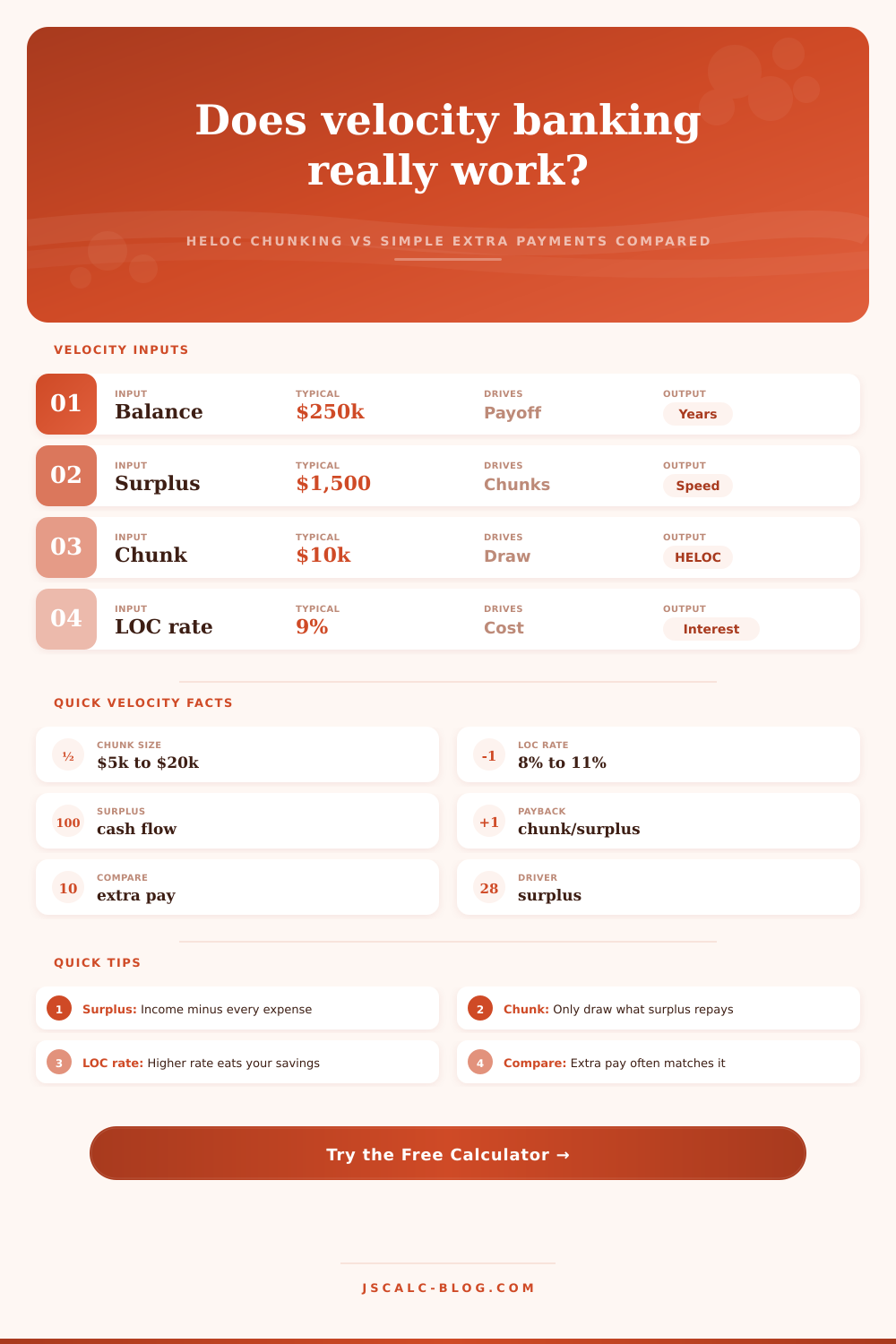

Your monthly surplus are the engine of this strategy. It is not some vague “live beneath your means” thing. It is the actual number that remains once all bills is paid, groceries, gas, and your savings goal. Velocity banking won’t help if you don’t have an excess from your paycheck each month. You must consistently have money left over each month before interest starts eating into the money meant for your savings.

The calculator above takes care of it. Input your surplus size and it’ll show you the new payoff timeline. It calculate the amortization schedules for you so you don’t have to put together some crazy spreadsheet to see if this works better than just making an extra principal payment.

The error starts with understanding the inputs. First, everyone plugs in what they think the inputs should be. “I’m going to put my current mortgage balance and interest rate.” No problem. Next, they estimate how much they spend each month. This has to be brutally honest. Don’t forget those little repairs, those meals out or subscriptions. Otherwise you’ll overestimate your surplus.

Overestimating your surplus means you draw too large a loan, which you won’t be able to repay soon enough. And that’s when the plan falls apart. Every day your line of credit balance exists, it’s accruing interest. Your mortgage is at six percent, while the line of credit are at nine percent. If you use higher-interest borrowing to pay off cheaper debt, you had better pay it off quickly. You need to save more in interest than you end up paying on the line of credit.

The idea is to “chunk” payments: Rather than paying extra every month in small increments, you allow your money to accrue in your checking account until reaching a target dollar amount, and apply that large sum toward the mortgage principal. Your principal balance drop immediately, causing your monthly interest charge to drop by the same amount for this month. To refill your checking account, you withdraw the equivalent amount from your line of credit. Now you’ve lowered your high-interest mortgage balance and kept your cash.

This continues until you notice that you owe that line of credit each month with the money you had leftover. You’re still making the same math-based extra payment, but now you’re also paying interest on the short-term loan. The tool also provides a handy comparison table. It lists simple extra payments and the velocity strategy side-by-side to show how each compares to the standard payoff time.

Notice that the time savings is generally small unless you have a large surplus of money. If your household’s cash flows aren’t extreme, throwing an additional amount at the principal each month will get you almost exactly as far, but you don’t run the danger of accumulating a spiral of revolving credit debt should life suddenly become more costly than expected.

And then there’s psychology. For others, the issue may simply be slow going. They aren’t able to watch their bank balance plummet. Which makes it hard for them to feel as though they’re doing anything. There’s something about watching a big chunk dissapears from their checking account and land in the mortgage principal column that gives them a sense of motion. Of being on board.

And if that’s enough to get (and keep) them on budget, great! Otherwise, that could be short; just a few months before the budget fades once again. But you don’t pay interest based off how you feel. The math matters, and you have to focus on the bottom line: what does this save over time?

If the income remains steady and the line of credit rate remains low, it will knock some number of years off a 30 year term. If you lose your job or rates skyrocket, then the revolving debt isn’t helping; it’s hurting. The bottom line: Velocity banking isn’t some secret loophole. It’s a variation of accelerated payoff… Which requires one additional step.

That added step increases risk and complexity. Before you draw a single dime, run your own numbers through the calculator. If your analysis reveals that velocity banking provides only incremental gains over simply paying slightly more every month, stick with the simple route. Personal finance rarely rewards complexity … except when it protects you from something costly. Simplicity typically wins here by allowing your surplus to do the heavy lifting for you.

You should of didn’t borrow against yourself to make a statement. Let the math tell its honest story.